jetcityimage

While Dollar General (NYSE:DG) has some nice growth opportunities ahead of it, its customer base continues to be impacted by a number of headwinds.

Company Profile

DG is one of the largest discount retailers in the U.S. The company offers a variety of items at its stores, with a focus on everyday necessities, including paper and cleaning products, packaged food, perishables, health & beauty, pets, and tobacco. Consumables represent nearly 80% of its sales. It also sells seasonal items, home products, and apparel, as well.

10-K

At the end of 2022, the company had over 19,000 stores located throughout the U.S. The company uses a small-store format, with 7,500 square feet of selling space, with new stores have about 8,500 square feet. DG is also starting to open its new pOpshelf concept, which is a small-box store focused on seasonal, home décor, beauty, party and entertainment supplies. It also opened its first Mi Súper Dollar General store in Mexico in February of 2023.

Opportunities & Risks

With over 19,000 stores, DG isn't exactly an expansion story per se, but new store openings is still an opportunity for the retailer. The company has over 3,000 retail projects slated in the U.S. this year, including 990 new stores and 2,000 remodels. Most remodels will be in its newer DGTP format, which adds cooler space and the ability to add fresh produce to stores. The company is also aggressively expanding its pOpshelf concept, while also starting to move into Mexico with its Mi Súper Dollar General concept. It plans to open 20 stores in northern Mexico this year, while opening 90 pOpshelf stores. It is looking to have 1,000 pOpshelf stores opened by the end of 2025.

Product expansion is another area of potential growth. Currently the company only offers fresh produce in just over 3,200 of its locations, so this is one area of growth as it adds coolers to more of its stores. Meanwhile, it is looking to expand its health offerings through its DG Wellbeing program, which adds 30% more selling space and 400 items. This was in 4,400 store at the end of 2022, with plans to be in 7,000 stores by the end of 2023. It's also testing some mobile health clinics in rural areas.

Margin expansion is another big opportunity. This can be achieved through such things as self-checkout, the expansion of its private tractor fleet, distribution and transportation efficiencies, improved global sourcing, as well as more private label offerings. The company is shifting to self-distribution of frozen and refrigerated goods, which should save costs and increase profitability. The company also has initiatives to reduce shrink and product damage.

DG is also trying to use its large customer base and data to help CPG companies advertise to its customer base through its DG Media Network. During its Q4 call, the company said it was seeing meaningful interest for CPG companies and that it expected this initiative to grow significantly in 2023.

When it comes to risks, the macroeconomy is first and foremost. The DG customer tends to be less affluent, and thus can be more impacted by macro and inflation headwinds. The company saw this in Q1, as its customers turned more towards private brands and items prices at or below a dollar.

In addition, during Q1 its customers appeared surprised by lower tax refunds, as things like the enhanced child tax credit and other popular tax breaks expired. In addition, there was an impact as states continued to pull back on emergency Covid-related SNAP benefits.

On its Q1 call, CEO Jeffery Own said:

Regarding tax refunds, we believe our customers were caught off-guard by the reduced amounts, which exacerbated the inflationary pressures they were already experiencing. Our customers typically use these refunds to repay debt, purchase big ticket items, make repairs, build a safety net in savings or a combination thereof. The changes this year are contributing to their financial insecurity, and many are using lower refunds to simply afford basic household essentials while others are contracting their overall spending. Turning to SNAP. As we mentioned on our Q4 2022 call, we did not see a notable sales impact in states that eliminated the emergency allotment early. Instead, our data suggests that customers who used SNAP simply made up the difference in their basket with another form of tender. However, in the states where reductions occurred in March of this year, we have seen an impact to sales as our customers appear to primarily have reduced the size of their basket instead of using other forms of tender to complete their purchases at the same level. Additionally, these and other customers appear to be shopping closer to payday. Finally, like other retailers, the cold and rainy weather also had a negative impact on our top line performance, particularly in March and April, which created a slow start to the spring season."

Insider Buying

In the wake of its post-earnings sell-off last quarter, DG's CEO and two directors picked up some shares on the open market. Owen bought shares for the first time, making a $237,000 purchase. Meanwhile, Chairman Michael Calbert laid out a cool $1.3 million to buy shares at an average price of $155.76. Calbert has been chairman since 2016, and has made three other purchases of the stock, but none since August 2016. Director Ann Maria Chadwick also spent $19,100 picking up shares as well.

I view the recent insider buying from the company's top two executives as a positive sign.

Valuation

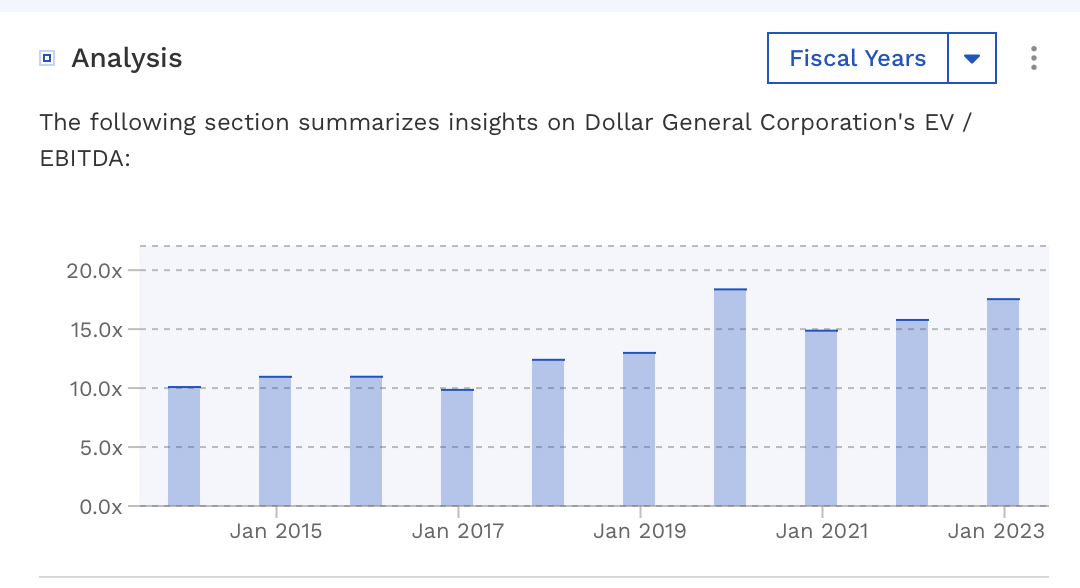

DG trades around 13.5x the FY2024 (ending January) consensus EBITDA of $4.0 billion and 12.6x the FY2025 consensus of $4.29 billion. From an EBITDAR perspective, it trades at around 9.5x FY 2024 estimates and 9x FY2025.

It trades at a forward P/E of 16.5x the FY24 consensus of $10.03. Based on 2025 analyst estimates of $10.96, it trades at just over 15x.

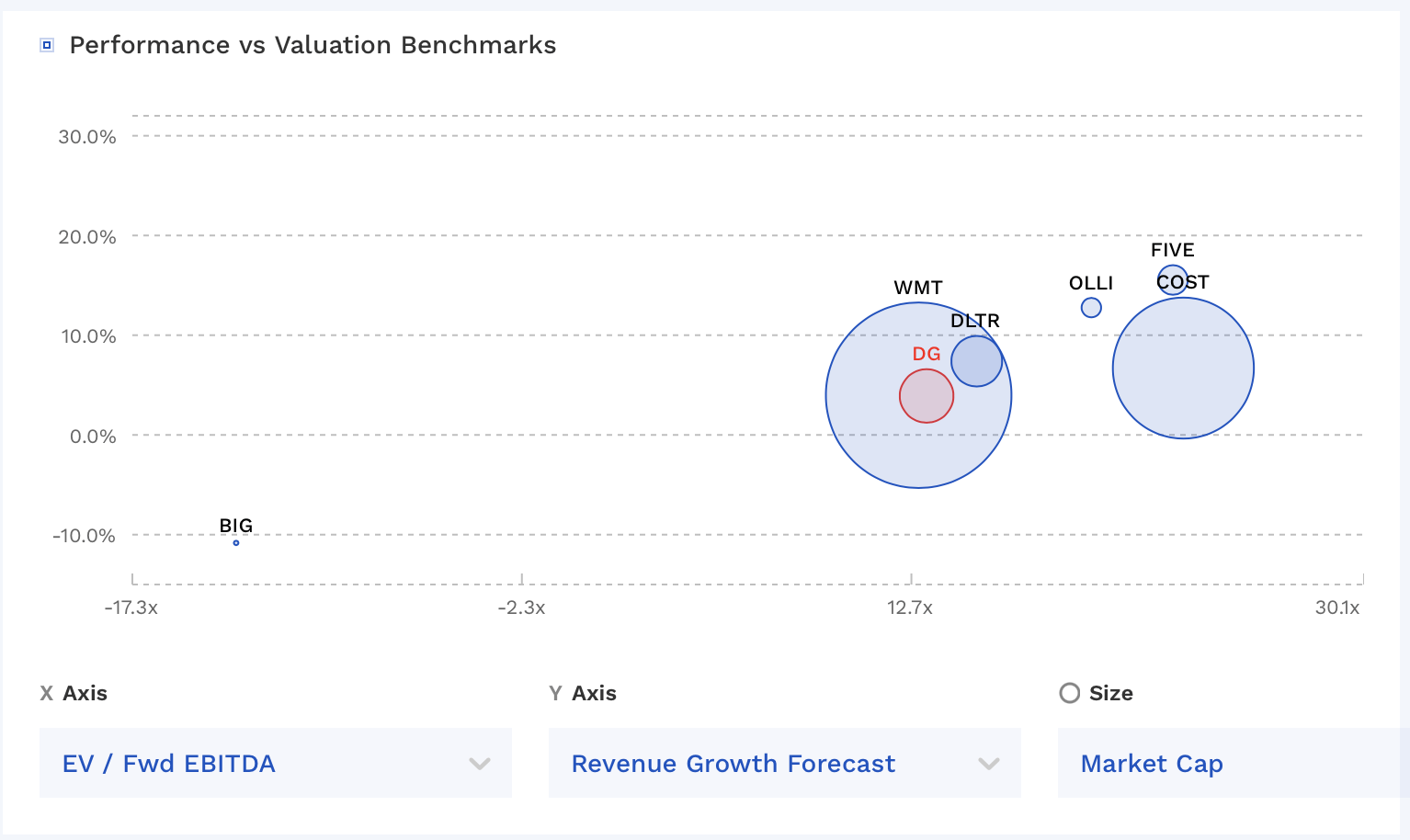

DG trades towards the lower end of other discount retailers, likely given its recent issues. Historically, the stock has traded at an EV/EBITDA of between 10-18.5x over the past several years.

DG Valuation Vs Peers (FinBox)

DG Historical Valuation (FinBox)

Conclusion

DG's most recent quarter caused the stock to lose some of its mystique as a defensive name. The retailer generally serves lower income customers, who have been hit with a number of headwinds, including lower tax refunds, the elimination of some SNAP benefits, inflation, higher interest rates, and a weaker general economy.

While the company has some nice growth opportunities ahead of it, many of these headwinds will likely persist in the near term. While the stock is well off its highs, its valuation is still generally above where it traded pre-pandemic. As such, I am currently neutral on the name. Longer term, the stock is worth watching and current investors should continue to hold their shares.

"general" - Google News

August 17, 2023 at 01:17PM

https://ift.tt/GfqVFNi

Dollar General: Customers Continue To See Headwinds (NYSE:DG) - Seeking Alpha

"general" - Google News

https://ift.tt/LpORdem

https://ift.tt/YyPaxrQ

Bagikan Berita Ini

0 Response to "Dollar General: Customers Continue To See Headwinds (NYSE:DG) - Seeking Alpha"

Post a Comment